IATA reports ups and downs in April air cargo and passenger demand

Image courtesy IATA

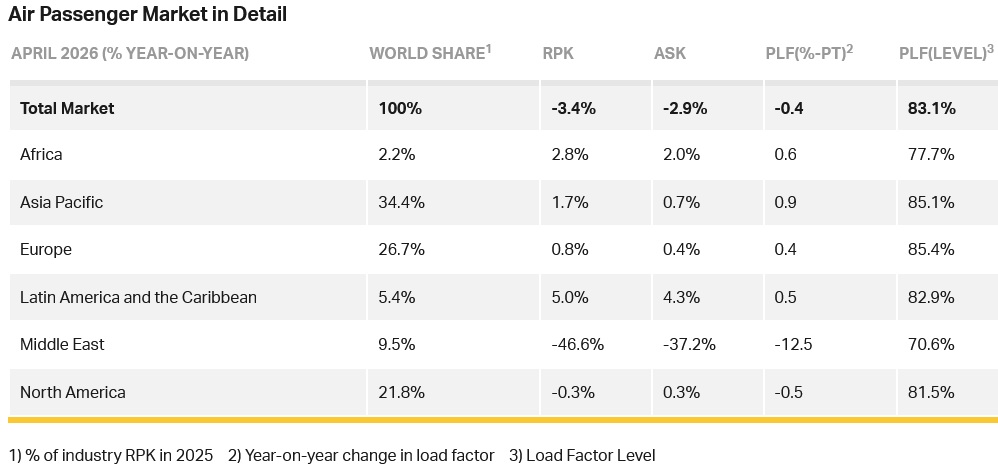

Total global passenger demand, measured in revenue passenger kilometres (RPK), was down -3.4% compared to April 2025. Excluding the Middle East, demand increased by 1.2%. Total capacity, measured in available seat kilometres (ASK), decreased -2.9% year-on-year. The load factor was 83.1% (-0.4 ppt compared to April 2025).

International demand fell -5.3% compared to April 2025. Excluding Middle East, demand grew by 1.9%. Capacity was down -5.1% year-on-year and the load factor was 83.9% (-0.2 ppt compared to April 2025).

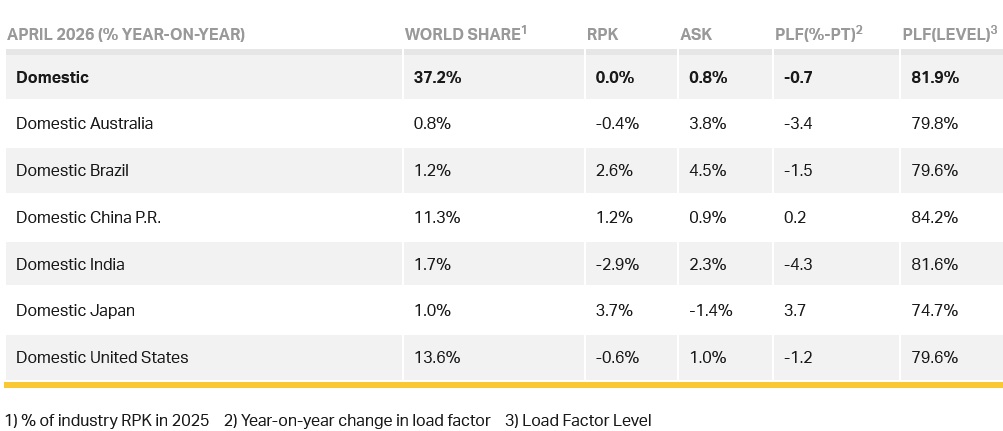

Domestic demand was flat compared to April 2025. Capacity increased 0.8% year-on-year. The load factor was 81.9% (-0.7 ppt compared to April 2025).

Willie Walsh (above), IATA’s Director General, said: “The 46.6% fall in demand for carriers in the Middle East due to war in the region was so acute that it dragged overall demand down -3.4%. The situation for air transport remains highly volatile. The cost of jet fuel more than doubled in April, which is pushing airfares up. Forward schedule data is showing a reduced offering in the coming months, indicating that airlines are balancing high fuel costs and weaker demand.”

Regional Breakdown - International Passenger Markets

International RPK fell -5.3%, with capacity falling -5.1%. However, this decline was caused by continuing heavy falls in demand for Middle East carriers. Excluding the Middle East, RPK increased by 1.9%. North America was flat and all other regions reported growth.

Asia-Pacific airlines achieved a 3.0% year-on-year increase in demand. Capacity increased 0.7% year-on-year, and the load factor was 87.5% (+1.9 ppt compared to April 2025), a record high for April. There was a notable slowdown in traffic on the Japan-China corridor, due to ongoing political tensions.

European carriers saw a 0.9% year-on-year increase in demand. Capacity increased 0.3% year-on-year, and the load factor was 84.9% (+0.6 ppt compared to April 2025). Direct traffic between Europe and Asia increased 15.3% as it replaced traffic transiting through the Middle East.

North American carriers saw a 0.0% year-on-year increase in demand. Capacity decreased -1.1% year-on-year, and the load factor was 83.9% (+0.9 ppt compared to April 2025).

Middle Eastern carriers saw a -48.1% year-on-year decrease in demand. Capacity fell -38.4% year-on-year, and the load factor was 70.1% (-13.1 ppt compared to April 2025). Traffic was impacted by the ongoing Iran war, though the decline slowed a little compared to March, as an uneasy ceasefire came into effect.

Latin American airlines achieved an 8.9% year-on-year increase in demand. Capacity climbed 7.2% year-on-year. The load factor was 84.6% (+1.4 ppt compared to April 2025).

African airlines saw a 2.2% year-on-year increase in demand. Capacity was up 1.2% year-on-year. The load factor was 77.9% (+0.7 ppt compared to April 2025).

Domestic Passenger Markets

Domestic RPK was flat in April compared to April 2025. Growth in Brazil, China, and Japan was balanced out by falls in Australia, India, and the United States. Load factors fell in most of the major markets barring China and Japan, though it should be noted that capacity in the Japanese market has declined for eight months in a row.

Air Cargo

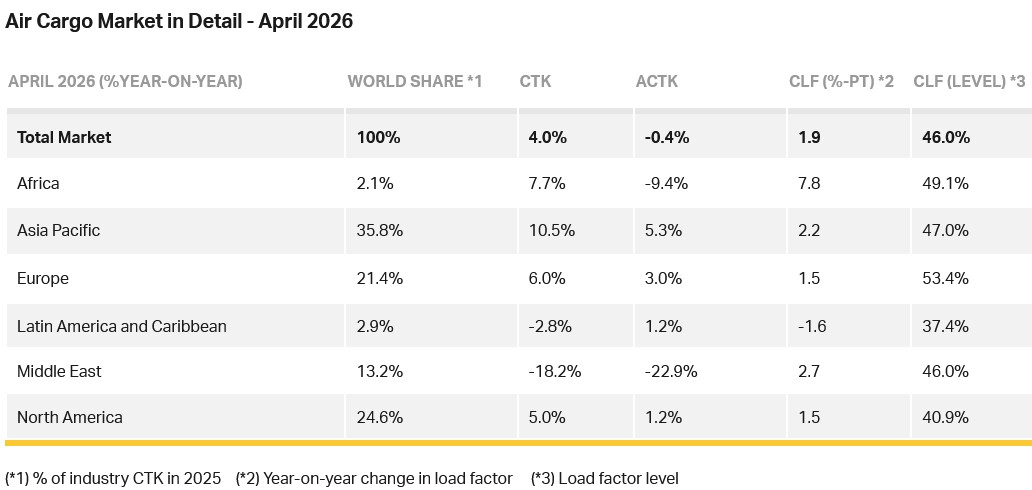

IATA's data for April 2026 global air cargo markets showed that total demand, measured in cargo tonne-kilometres (CTK), increased by 4.0% compared to April 2025 levels (+4.0% for international operations). Capacity, measured in available cargo tonne-kilometres (ACTK), decreased by -0.4% compared to April 2025 (-0.9% for international operations).

Willie said: “Air cargo demand grew 4% year-on-year in April, driven by strong Asia-linked trade flows. But this positive news masks a more complex operating environment. Severe disruption at major Gulf hubs due to the war in the Middle East continued to reshape trade routes and constrain capacity on key corridors. With dedicated freighters carrying much of the growth, air cargo is once again keeping supply chains moving amid trade disruptions. The coming months will test how well the sector can absorb continued geopolitical uncertainty and elevated operating costs.”

Several factors in the operating environment should be noted:

- Global trade contracted in March by 2.1% month-on-month after four consecutive months of growth, highlighting the continued vulnerability of trade momentum to geopolitical shocks.

- Jet fuel prices rose sharply in April, up 121.1% year-on-year, alongside a 77.7% increase in crude oil prices.

- Global manufacturing sentiment remained in growth territory in April, strengthening from March. The Purchasing Managers’ Index (PMI) rose 1.9 points to 53.4, while the PMI for new export orders reached 50.2. With both indicators above the 50-point expansion threshold, conditions remain supportive for air cargo demand.

April Regional Performance

Asia-Pacific airlines saw a 10.5% year-on-year growth in air cargo demand in April, the strongest rise of all regions. Capacity increased by 5.3% year-on-year.

North American carriers saw a 5.0% year-on-year increase in air cargo demand in April. Capacity increased by 1.2% year-on-year.

European carriers saw a 6.0% year-on-year increase in demand for air cargo in April. Capacity increased by 3.0% year-on-year.

Middle Eastern carriers saw a -18.2% year-on-year decrease in demand for air cargo in April, the weakest performance of all regions. Capacity decreased by -22.9% year-on-year.

Latin American and Caribbean carriers saw a -2.8% year-on-year decrease in demand for air cargo in April. Capacity increased by 1.2% year-on-year.

African airlines saw a 7.7% year-on-year increase in demand for air cargo in April. Capacity decreased by -9.4% year-on-year.

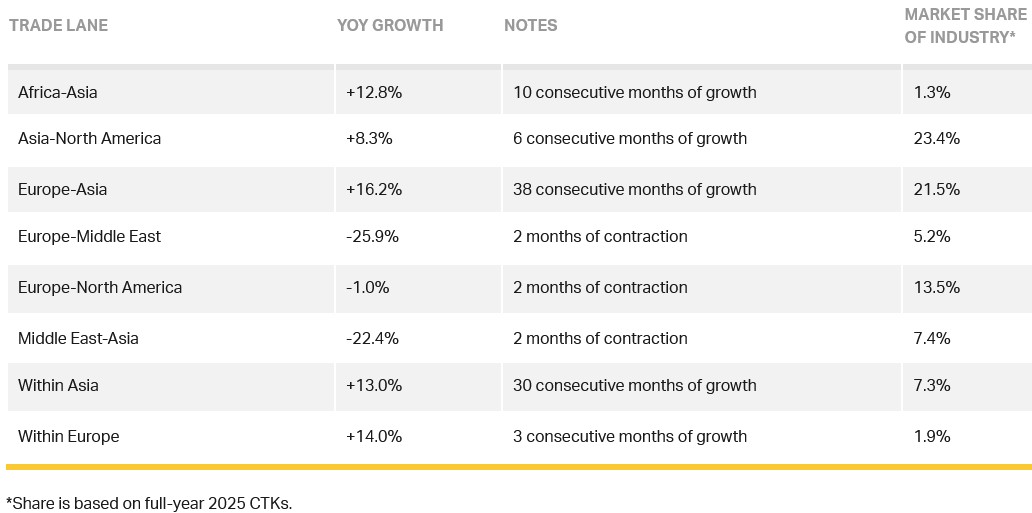

Trade Lane Growth

Air cargo performance diverged across major trade lanes in April. Africa–Asia led growth followed by Asia–Europe, with intra-Asia also holding strong on regional trade. In contrast, Gulf-linked corridors were severely disrupted by the ongoing conflict in the Middle East.