IATA reports continued air travel and cargo recovery

Image courtesy IATA

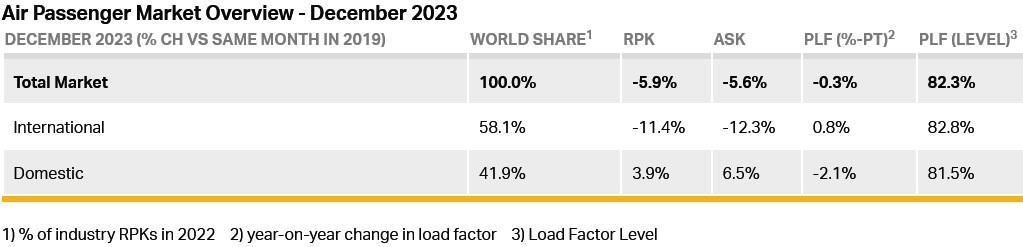

Total traffic in 2023 (measured in revenue passenger kilometres or RPKs) rose 36.9% compared to 2022. Globally, full year 2023 traffic was at 94.1% of pre-pandemic (2019) levels. December 2023 total traffic rose 25.3% compared to December 2022 and reached 97.5% of the December 2019 level. Fourth quarter traffic was at 98.2% of 2019, reflecting the strong recovery towards the end of the year.

International traffic in 2023 climbed 41.6% versus 2022 and reached 88.6% of 2019 levels. December 2023 international traffic climbed 24.2% over December 2022, reaching 94.7% of the level in December 2019. Fourth quarter traffic was at 94.5% of 2019.

Domestic traffic for 2023 rose 30.4% compared to the prior year. Last year's domestic traffic was 3.9% above the full year 2019 level. December 2023 domestic traffic was up 27.0% over the year earlier period and was at 2.3% above December 2019 traffic. Fourth quarter traffic was 4.4% higher than the same quarter in 2019.

Willie Walsh (above), IATA’s Director General, said: “The strong post-pandemic rebound continued in 2023. December traffic stood just 2.5% below 2019 levels, with a strong performance in quarter four, teeing-up airlines for a return to normal growth patterns in 2024.

"The recovery in travel is good news. The restoration of connectivity is powering the global economy as people travel to do business, further their educations, take hard-earned vacations and much more. But to maximise the benefits of air travel in the post-pandemic world, governments need to take a strategic approach. That means providing cost-efficient infrastructure to meet demand, incentivising Sustainable Aviation Fuel (SAF) production to meet our net zero carbon emission goal by 2050, and adopting regulations that deliver a clear cost-benefit.

"Completing the recovery must not be an excuse for governments to forget the critical role of aviation to increasing the prosperity and well-being of people and businesses the world over.”

International Passenger Markets

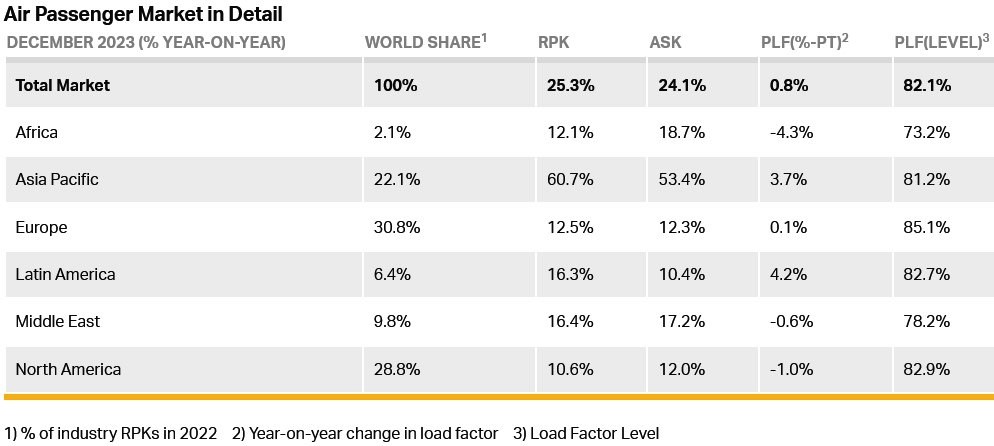

Asia-Pacific airlines posted a 126.1% rise in full year international 2023 traffic compared to 2022, maintaining the strongest year-over-year rate among the regions. Capacity rose 101.8% and the load factor climbed 9.0 percentage points to 83.1%. December 2023 traffic rose 56.9% compared to December 2022.

European carriers’ full year traffic climbed 22.0% versus 2022. Capacity increased 17.5%, and load factor rose 3.1 percentage points to 83.8%. For December, demand climbed 13.6% compared to the same month in 2022. December traffic was higher than the corresponding month in 2019 for the first time since the start of the pandemic.

Middle Eastern airlines saw a 33.3% traffic rise in 2023 compared to 2022. Capacity increased 26.0% and load factor climbed 4.4 percentage points to 80.1%. December demand climbed 16.6% compared to the same month in 2022.

North American carriers reported a 28.3% annual traffic rise in 2023 compared to 2022. Capacity increased 22.4%, and load factor climbed 3.9 percentage points to 84.6%. December 2023 traffic rose 13.5% compared to the year-ago period.

Latin American airlines posted a 28.6% traffic rise in 2023 over full year 2022. Annual capacity climbed 25.4% and load factor increased 2.1 percentage points to 84.7%, the highest among the regions. December demand climbed 26.5% compared to December 2022.

African airlines’ annual traffic rose 38.7% in 2023 versus the prior year. Full year 2023 capacity was up 38.3% and load factor climbed 0.2 percentage points to 71.9%, the lowest among regions. December 2023 traffic for African airlines rose 9.5% over December 2022.

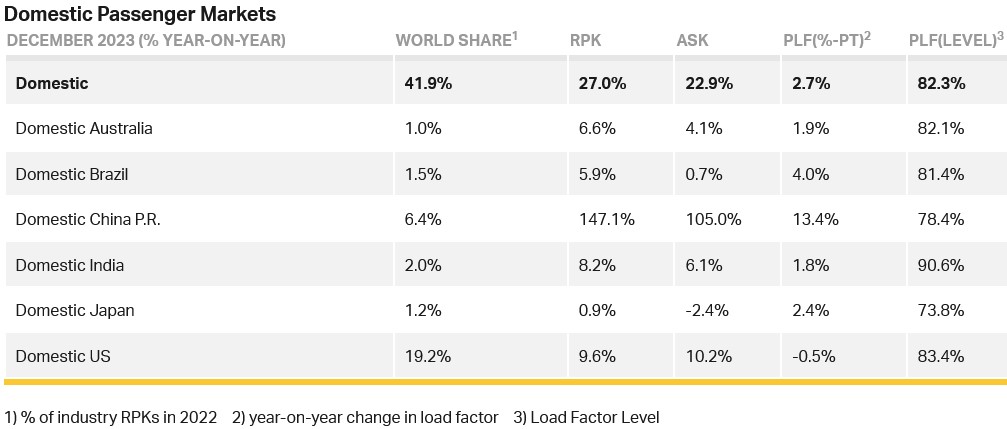

China’s full year domestic traffic rose 138.8% versus 2022 and is now 7.1% above the 2019 level.

Australia (-4.2% compared to 2019) and Japan (-3.2% compared to 2019) are the only major domestic markets yet to recover pre-pandemic traffic demand.

Walsh said: “Our push to connect our world even more strongly than before the pandemic must not come at the expense of our environment. The industry’s goal to reach net zero CO2 emissions by 2050 remains steadfast. To accelerate the transition, we need governments and fuel suppliers to step up and do more. We saw a strong increase in the use of SAF in 2023 but SAF is still only 3% of all global renewable fuels production. That is unacceptable.

"Aircraft have no option but to rely on liquid fuels, whereas other transport modes have alternatives. A massive collective effort is needed to increase SAF output as a proportion of overall renewable fuel production as quickly as possible.”

Air Cargo

IATA data for global air freight markets showed that air cargo demand rebounded in 2023 with a particularly strong fourth quarter performance despite economic uncertainties. Full-year demand reached a level just slightly below 2022 and 2019.

Global full-year demand in 2023, measured in cargo tonne-kilometers (CTKs), was down 1.9% compared to 2022 (-2.2% for international operations). Compared to 2019, it was down 3.6% (-3.8 for international operations).

Capacity in 2023, measured in available cargo tonne-kilometers (ACTKs), was 11.3% above 2022 (+9.6% for international operations). Compared to 2019 (pre-COVID) levels, capacity was up 2.5% (0.0% for international operations).

December 2023 saw an exceptionally strong performance: global demand was 10.8% above 2022 levels (+11.5% for international operations). This was the strongest annual growth performance over the past two years. Global capacity was 13.6% above 2022 levels (+14.1% for international operations).

Some indicators to note include:

- Global cross-border trade recorded growth for the third consecutive month in October, reversing its previous downward trend.

- December inflation in both the United States and the EU as measured by the corresponding Consumer Price Indices (CPI) stayed below 3.5% year-on-year. China’s CPI, however, indicated deflation for the third consecutive month, raising concerns of an economic slowdown.

- Both the manufacturing output and new export order Purchasing Managers Indexes (PMIs) – two leading indicators of global air cargo demand—continued to hover below the 50-mark in December, usual markers for contraction.

Walsh said: “Despite political and economic challenges, 2023 saw air cargo markets regain ground lost in 2022 after the extraordinary COVID peak in 2021. Although full year demand was shy of pre-COVID levels by 3.6%, the significant strengthening in the last quarter is a sign that markets are stabilising towards more normal demand patterns. That puts the industry on very solid ground for success in 2024. But with continued and in some cases intensifying, instability in geopolitics and economic forces, little should be taken for granted in the months ahead.”

December Regional Performance (Total Market)

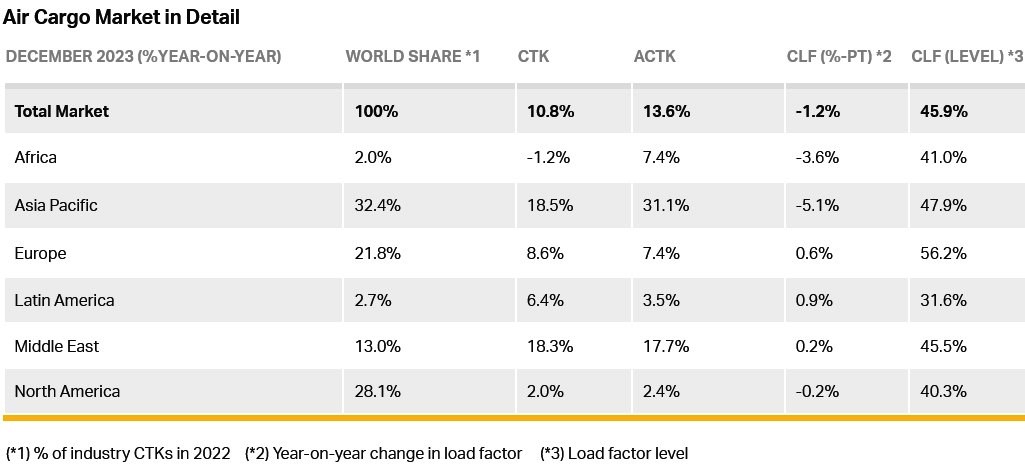

Asia-Pacific airlines posted a 0.9% increase in demand in 2023 compared to 2022 (-1.4% for international operations) and a capacity increase of 28.5% (+16.6% for international operations). In December, airlines in the region recorded the best performance of all regions, posting an 18.5% increase in demand (+15.4% for international operations) compared to 2022. Capacity increased 31.1% (+22.9% for international operations) during the same period.

North American carriers reported the worst year-on-year performance of all regions, with a 5.7% decrease in demand in 2023 compared to 2022 (-4.3% for international operations) and a capacity increase of 0.3% (+2.7% for international operations). In December airlines in the region reported a 2.0% decrease in demand (+5.9% international operations), compared to 2022. Capacity increased 2.4% (+8.5% for international operations) during the same period.

European carriers posted a 3.9% decrease in demand in 2023 compared to 2022 (-4.1% for international operations). During the same period, airlines posted a capacity increase of 4.5% for both global and international operations. In December, airlines in the region posted an 8.6% increase in demand (+8.7% for international operations) compared to 2022. Capacity increased 7.4% (+7.5% for international operations) during the same period. Airlines in the region continued to be most affected by the war in Ukraine.

Middle Eastern carriers reported an increase in demand of 1.6% for global and international demand in 2023 compared to 2022 and an increase in capacity of 13.5% (+13.6% for international operations). In December airlines in the region posted an 18.3% increase in demand for both global and international operations compared to 2022. Capacity increased 17.7% (+17.8% for international operations) during the same period.

Latin American carriers posted the strongest year-on-year performance of all regions, with a 2.0% increase in demand in 2023 compared to 2022 (+1.9% for international operations). During the same period, airlines posted a capacity increase of 13.2% (+16.9% for international operations). In December airlines in the region posted growth in demand of 6.4% (+6.3% for international operations) compared to 2021. Capacity grew 3.5% (+4.2% for international operations) during the same period.

African airlines reported a decrease in demand of 1.8% (-2.0% for international demand) in 2023 compared to 2022 and an increase in capacity of 5.6% (+5.0% for international operations). In December airlines in the region posted the weakest performance of all with a 1.2% decrease in demand (-1.4% for international operations) compared to 2021. Capacity grew 7.4% (+6.8% for international operations) during the same period.

Red Sea Disruption

In November and December air cargo experienced a modest rise in demand and yields due to disruptions in the Red Sea. The following was observed when comparing data for the week commencing 4th November 2023 and the week ending 9th December 2023:

- A 1% increase in global air cargo demand coupled with a 5% rise in yields;

- In the Asia-Pacific region, demand grew by 2% and yields by 6%;

- A 1% increase in demand between China and the rest of the world and an 11% increase in yields;

- Europe's demand remained steady, but yields increased by 3%;

- In the Middle East, demand was constant with a 4% rise in yields.

Data for the last half of December showed a normalisation of demand and yields.

Walsh said: "The recent disruption to maritime routes in the Red Sea has seen some shippers pivot to air cargo. The increased demand saw a spike in air cargo yields on related trade lanes. A similar spike is expected in January as disruptions intensified.

"While not all cargo is suitable for air transport, it is a vital option for some of the most urgent shipments in extraordinary circumstances. And that is critical to the continuity of the global economy."