May's air passenger demand down whilst air cargo demand rises

Image courtesy IATA

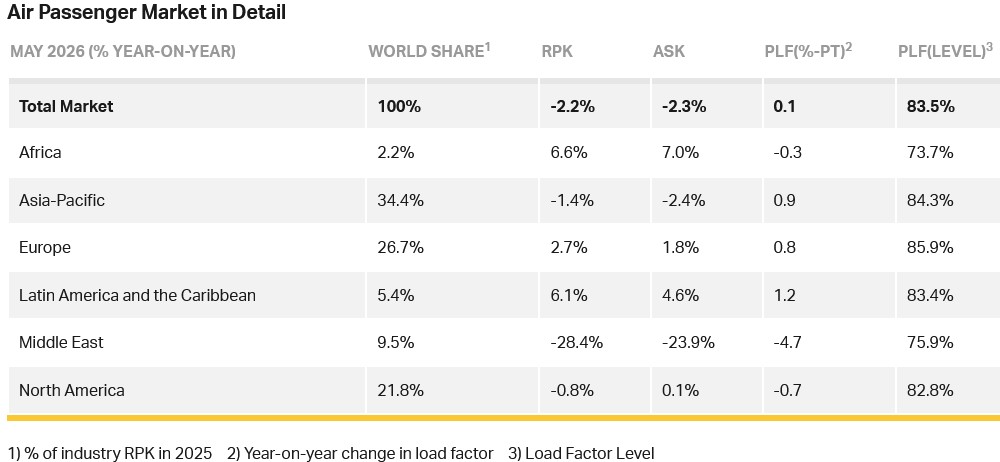

Total passenger demand, measured in revenue passenger kilometres (RPK), was down 2.2% compared to May 2025. Excluding the Middle East, demand grew by 0.7%. Total capacity, measured in available seat kilometres (ASK), decreased 2.3% year-on-year. The load factor was 83.5% (+0.1 ppt compared to May 2025), a record high for May.

International demand fell 1.6% compared to May 2025. Excluding the Middle East, demand grew by 3.1%. Capacity was down 2.4% year-on-year and the load factor was 83.7% (+0.7 ppt compared to May 2025).

Domestic demand contracted 3.1% compared to May 2025. Capacity decreased 2.1% year-on-year. The load factor was 83.0% (-0.8 ppt compared to May 2025).

Willie Walsh (above), IATA’s Director General said: “Air passenger demand was down 2.2% year-on-year in May on the impact of war in the Middle East. The decline was centered on carriers in the Middle East with a 28.4% year-on-year fall. That’s a significant improvement on the 46.6% decline recorded for April, a sign of the region’s resilience. Notably, we also saw year-on-year contractions in demand in both North America and Asia, largely related to domestic market conditions in the US and China.

Overall, May demand still appeared to be largely resilient in the face of high fuel prices and air fares. While the recent sharp drop in oil prices is an encouraging development, the challenges created by the war will likely persist for some time. Oil supply through the Strait of Hormuz remains uncertain and it is likely to take time before the benefit of lower oil prices is reflected in ‘normalised’ jet fuel pricing. In the meantime, airlines who are operating on a 2.0% margin will have little choice but to continue testing demand resilience with higher fares that attempt to cover elevated fuel costs.”

Regional Breakdown - International Passenger Markets

International RPK fell 1.6%, with capacity falling 2.4%. The pace of decline reduced compared to April and many regions hit record load factors for May, with only the Middle East posting a load factor decline.

Asia-Pacific airlines achieved a 1.3% year-on-year increase in demand. Capacity decreased 1.1% year-on-year, and the load factor was 85.3% (+2.0 ppt compared to May 2025). In Vietnam, tighter limits on jet fuel imports led to significant capacity cuts on short haul routes, resulting in a decline in intra-Asia international traffic during the month.

European carriers saw a 3.8% year-on-year increase in demand. Capacity increased 2.3% year-on-year, and the load factor was 85.4% (+1.2 ppt compared to May 2025). Of note is the 15% increase in direct traffic to Asia, reflecting a continued shift to direct services between the two regions.

North American carriers increased demand 1.0% year-on-year. Capacity increased 0.6% year-on-year, and the load factor was 84.0% (+0.4 ppt compared to May 2025).

Middle Eastern carriers saw a 28.8% year-on-year decrease in demand. Capacity fell 24.3% year-on-year, and the load factor was 76.1% (-4.8 ppt compared to May 2025). The impacts of the Iran war continue to cause a highly negative year-on-year traffic comparison, but month-to-month the impact is lessening and the rate of decline was almost half that of April.

Latin American airlines achieved a 10.5% year-on-year increase in demand. Capacity climbed 9.0% year-on-year. The load factor was 85.0% (+1.2% ppt compared to May 2025).

African airlines saw an 8.9% year-on-year increase in demand. Capacity was up 8.3% year-on-year. The load factor was 73.4% (+0.4 ppt compared to May 2025).

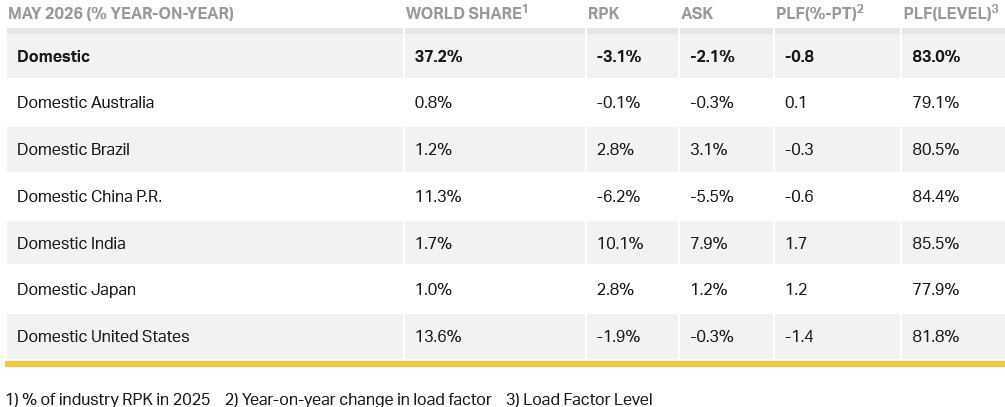

Domestic Passenger Markets

Domestic RPK fell (-3.1%) in May 2026 compared to the same month last year, with the largest fall in China, which may be linked to higher fares and/or the Dragon Boat Festival occurring in June this year. The US also had a notable decline while most other markets achieved moderate growth.

Air Cargo

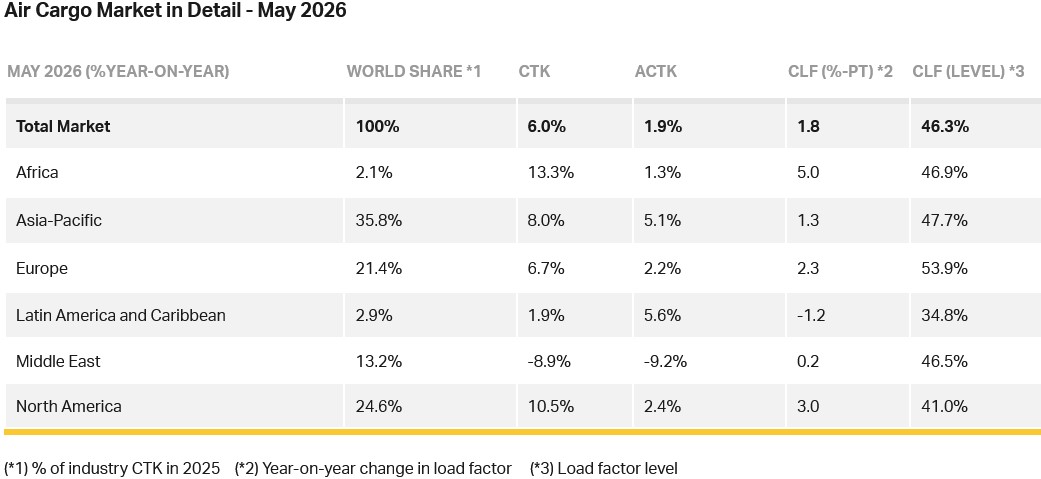

IATA data for global air cargo markets in May 2026 showed total demand, measured in cargo tonne-kilometres (CTK), increased by 6.0% compared to May 2025 levels (6.5% for international operations). Capacity, measured in available cargo tonne-kilometres (ACTK), increased by 1.9% compared to May 2025 (2.8% for international operations).

Willie said: “Air cargo demand grew 6% year-on-year in May, with Africa, Asia-Pacific, Europe, and North American regions all reporting above trend growth. Carriers in the Middle East, however, reported a combined contraction of 8.9% year-on-year as war-related impacts continued.

May’s strong performance coupled with macro-economic factors give cautious optimism for air cargo’s prospects over the remainder of the year. Trade and manufacturing output are both growing. Airlines have adapted operations to align with shifting demand patterns and supply chain needs. Meanwhile, yield growth and higher load factors are helping to recoup higher fuel costs. It’s still a tough year, particularly as Middle East uncertainties weigh heavily on parts of the industry, but robust demand and airline resilience are clear.”

Several factors in the operating environment should be noted:

- Global trade increased by 5.0% year-on-year, extending 25 months of consecutive annual growth.

- Jet fuel prices fell by 16.3% month-on-month in May but remained 93.5% above year-earlier levels.

- Global manufacturing activity remained supportive in May, but export orders weakened. The Global Manufacturing Output Purchasing Managers’ Index (PMI) rose to 53.5, while the New Export Orders Index stayed below the 50-mark at 49.6, suggesting air cargo growth was supported by selected trade flows rather than a broad-based rise in global exports.

Asia-Pacific airlines saw an 8.0% year-on-year growth in air cargo demand in May. Capacity increased by 5.1% year-on-year.

North American carriers saw a 10.5% year-on-year increase in air cargo demand in May. Capacity increased by 2.4% year-on-year.

European carriers saw a 6.7% year-on-year increase in demand for air cargo in May. Capacity increased by 2.2% year-on-year.

Middle Eastern carriers saw an 8.9% year-on-year decrease in demand for air cargo in May, the weakest performance of all regions. Capacity decreased by 9.2% year-on-year.

Latin American and Caribbean carriers saw a 1.9% year-on-year increase in demand for air cargo in May. Capacity increased by 5.6% year-on-year.

African airlines saw a 13.3% year-on-year increase in demand for air cargo in May, the strongest performance of all regions. Capacity increased by 1.3% year-on-year.

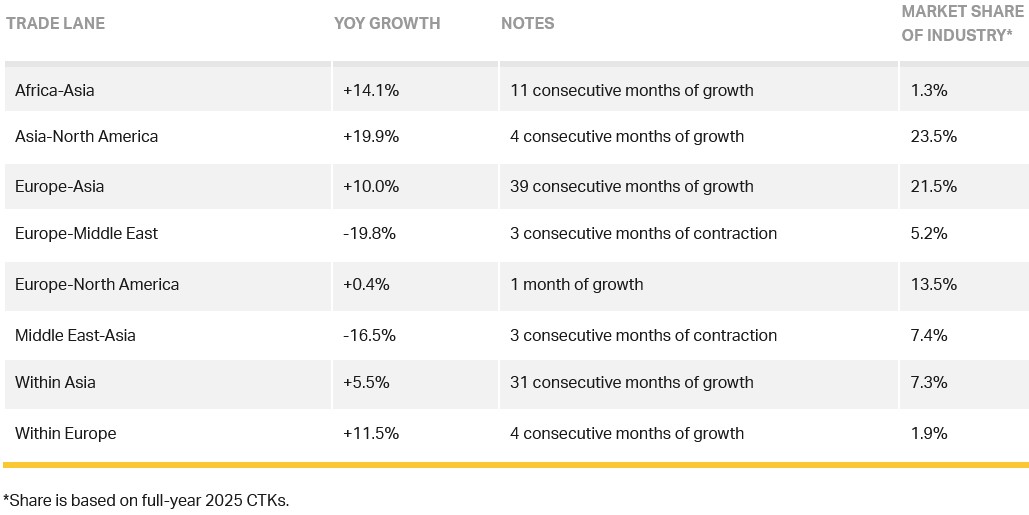

Trade Lane Growth

Air cargo performance diverged across major trade lanes in May. Asia-North America led growth followed by Africa-Asia, intra-Europe and Europe-Asia. In contrast, Gulf-linked corridors were still severely disrupted by the ongoing conflict in the Middle East.