IATA sees passenger demand down and air cargo up in February

Above:

Willie Walsh, Director General, International Air Transport Association.

Courtesy IATA

Because comparisons for passenger demand between 2021 and 2020 monthly results are distorted by the extraordinary impact of COVID-19, unless otherwise noted all comparisons are to February 2019, which followed a normal demand pattern.

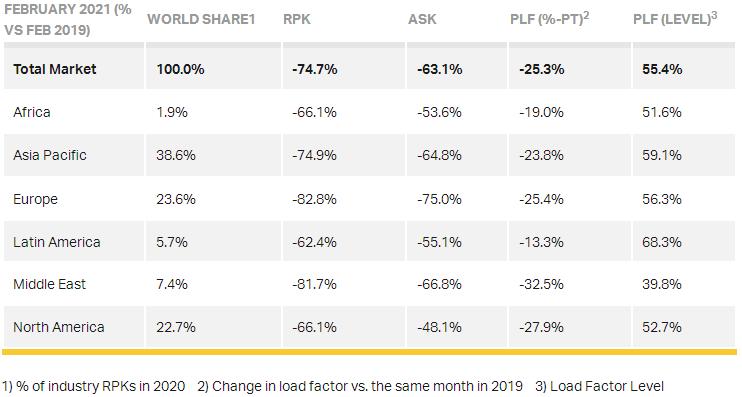

Total demand for air travel in February 2021 (measured in revenue passenger kilometres or RPKs) was down 74.7% compared to February 2019. That was worse than the 72.2% decline recorded in January 2021 versus two years ago.

International passenger demand in February was 88.7% below February 2019, a further drop from the 85.7% year-to-year decline recorded in January and the worst growth outcome since July 2020. Performance in all regions worsened compared to January 2021.

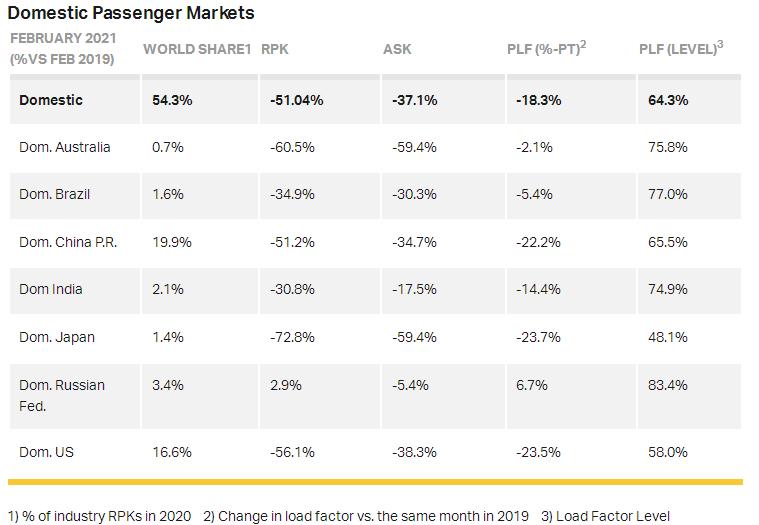

Total domestic demand was down 51.0% versus pre-crisis (February 2019) levels. In January it was down 47.8% on the 2019 period. This largely was owing to weakness in China travel, driven by government requests that citizens stay at home during the Lunar New Year travel period.

“February showed no indication of a recovery in demand for international air travel. In fact, most indicators went in the wrong direction as travel restrictions tightened in the face of continuing concerns over new coronavirus variants. An important exception was the Australian domestic market. A relaxation of restrictions on domestic flying resulted in significantly more travel. This tells us that people have not lost their desire travel. They will fly, provided they can do so without facing quarantine measures,” said Willie Walsh, IATA’s Director General.

International Passenger Markets

Asia-Pacific airlines’ February traffic was down 95.2% compared to February 2019, little changed from the 94.8% decline registered for January 2021 compared to January 2019. The region continued to suffer from the steepest traffic declines for an eighth consecutive month. Capacity was down 87.5% and the load factor sank 50.0 percentage points to 31.1%, the lowest among regions.

European carriers recorded an 89.0% decline in traffic in February versus February 2019, substantially worse than the 83.4% decline in January compared to the same month in 2019. Capacity sank 80.5% and load factor fell by 36.0 percentage points to 46.4%.

Middle Eastern airlines saw demand fall 83.1% in February compared to February 2019, worsened from an 82.1% demand drop in January, versus the same month in 2019. Capacity fell 68.6%, and load factor declined 33.4 percentage points to 39.0%.

North American carriers’ February traffic sank 83.1% compared to the 2019 period, a deterioration from a 79.2% decline in January year to year. Capacity sagged 63.9%, and load factor dropped 41.9 percentage points to 36.7%.

Latin American airlines experienced an 83.5% demand drop in February, compared to the same month in 2019, markedly worse than the 78.5% decline in January 2019. February capacity was 75.4% down compared to February 2019 and load factor dropped 26.7 percentage points to 54.6%, highest among the regions for a fifth consecutive month.

African airlines’ traffic dropped 68.0% in February versus February two years ago, which was a setback compared to a 66.1% decline recorded in January compared to January 2019. February capacity contracted 54.6% versus February 2019, and load factor fell 20.5 percentage points to 49.1%.

Australia’s domestic traffic was down 60.5% in February compared to February 2019, dramatically improved compared to the 77.3% decline in January over 2019. Some state border restrictions were eased in early February.

US domestic traffic declined 56.1% in February versus the same month in 2019, improved from the 58.4% decline in January compared to two years ago. The improvement was driven by falling rates of contagion and accelerating vaccinations.

Walsh said: “The US Centers for Disease Control and Prevention (CDC) recently stated that vaccinated individuals can travel safely. That is good news. We have also recently seen Oxera-Edge Health research highlighting the efficacy of fast, accurate and affordable rapid tests for COVID-19. These developments should reassure governments that there are ways to efficiently manage the risks of COVID-19 without relying on demand-killing quarantine measures and/or expensive and time-consuming PCR testing.

“Two key components for an efficient restart of travel need to be urgently progressed. The first is the development of global standards for digital COVID-19 test and/or vaccination certificates. The second is government agreement to accept certificates digitally. Our experiences to date already demonstrate that paper-based systems are not a sustainable option. They are vulnerable to fraud. And, even with the limited amount of flying today, the check-in process needs pre-COVID-19 staffing levels just to handle the paperwork.

"Paper processes will not be sustainable when travel ramps up. The IATA Travel Pass app was developed precisely in anticipation of this need to manage health credentials digitally. Its first full implementation trial is focused on Singapore, where the government has already announced that it will accept health certificates through the app. This will be an essential consideration for all governments when they are ready to relink their economies with the world through air travel.”

Air Cargo

Data for global air cargo markets showing that air cargo demand continued to outperform pre-COVID levels with demand up 9% over February 2019. February demand also showed strong month-on-month growth over January 2021 levels. Volumes have now returned to 2018 levels seen prior to the US-China trade war.

Because comparisons between 2021 and 2020 monthly results are distorted by the extraordinary impact of COVID-19, unless otherwise noted all comparisons to follow are to February 2019 which followed a normal demand pattern.

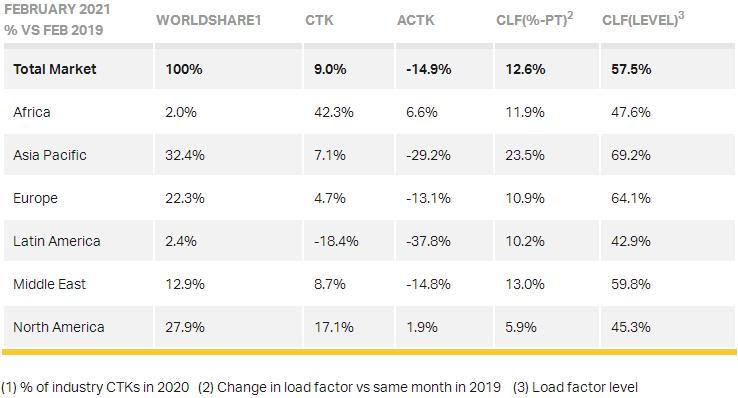

Global demand, measured in cargo tonne-kilometres (CTKs*), was up 9% compared to February 2019 and +1.5% compared to January 2021. All regions except for Latin America saw an improvement in air cargo demand compared to pre-COVID levels and North America and Africa were the strongest performers.

The recovery in global capacity, measured in available cargo tonne-kilometers (ACTKs), stalled owing to new capacity cuts on the passenger side as governments tightened travel restrictions due to the recent spike in COVID-19 cases. Capacity shrank 14.9% compared to February 2019.

The operating conditions remain supportive for air cargo:

- Conditions in the manufacturing sector are robust despite the recent spike in COVID-19 outbreaks. The global manufacturing Purchasing Managers’ Index (PMI) was at 53.9 in February. Results above 50 indicate manufacturing growth versus the prior month.

- The new export orders component of the manufacturing PMI – a leading indicator of air cargo demand– picked up compared to January.

- Supply chain disruptions and the resulting delivery delays have led to long supplier delivery times – the second longest in the history of the manufacturing PMI. This typically means manufacturers use air transport, which is quicker, to recover time lost during the production process.

- The level of inventories remains relatively low compared to sales volumes. Historically, this has meant that businesses had to quickly refill their stocks, for which they also used air cargo.

“Air cargo demand is not just recovering from the COVID-19 crisis, it is growing. With demand at 9% above pre-crisis levels (Feb 2019), one of the main challenges for air cargo is finding sufficient capacity. This makes cargo yields a bright spot in an otherwise bleak industry situation. It also highlights the need for clarity on government plans for a safe industry restart.

"Understanding how passenger demand could recover will indicate how much belly capacity will be available for air cargo. Being able to efficiently plan that into air cargo operations will be a key element for overall recovery,” said Mr Walsh.

February Regional Performance

Asia-Pacific airlines saw demand for international air cargo rise 10.5% in February 2021 compared to the same month in 2019. As the main global manufacturing hub, the region has benefited from the pickup in economic activity. Demand in the majority of the region’s key international trade lanes has returned to pre-COVID-19 levels. International capacity remained constrained in the region, down 23.6% versus February 2019. The region’s airlines reported the highest international load factor at 77.4%.

North American carriers posted a 17.4% increase in international demand in February compared to February 2019. Economic activity in the US continues to recover, supported by the rising demand for e-commerce amid lockdown restrictions. Demand grew 39% on the Asia – North America route vs February 2019. The business environment for air cargo remains supportive; the $1,400 stimulus checks to US households will likely drive further growth in e-commerce and the level of inventories remains relatively low compared to sales volumes. Historically, this has meant that businesses had to quickly re-stock for which they also used air cargo. International capacity grew by 4.4% in February compared to 2019.

European carriers posted a 4.7% increase in demand in February compared to same month in 2019. Cargo demand was largely unaffected by the new lockdowns in Europe and the operating conditions remain supportive for air cargo. International capacity decreased by 12.5% in February,

Middle Eastern carriers posted an 8.8% rise in international cargo volumes in February versus February 2019. Of the region’s key international routes, Middle East-Asia and Middle East-North America have provided the most significant support, rising 27% and 17% respectively in February compared to February 2019. February capacity was down 14.9% compared to the same month in 2019.

Latin American carriers reported a decline of 20.5% in international cargo volumes in February compared to the 2019 period; this was a deterioration from January when demand was down the 17.5% on 2019 levels. Drivers of air cargo demand in Latin America remain relatively less supportive than in the other regions. International capacity decreased 43.0% compared to February 2019. Weakness within the Central and South America markets, which dropped around 40% compared to February 2019, continued to outweigh the full recovery seen on North – Central America routes, which saw levels increase 10% compared to February 2019 levels.

African airlines’ cargo demand in February increased a massive 44.2% compared to the same month in 2019the strongest of all regions. Robust expansion on the Asia-Africa trade lanes contributed to the strong growth. February international capacity grew by 9.8% compared to February 2019.