IATA reports continued passenger and cargo recovery in October

Image courtesy IATA

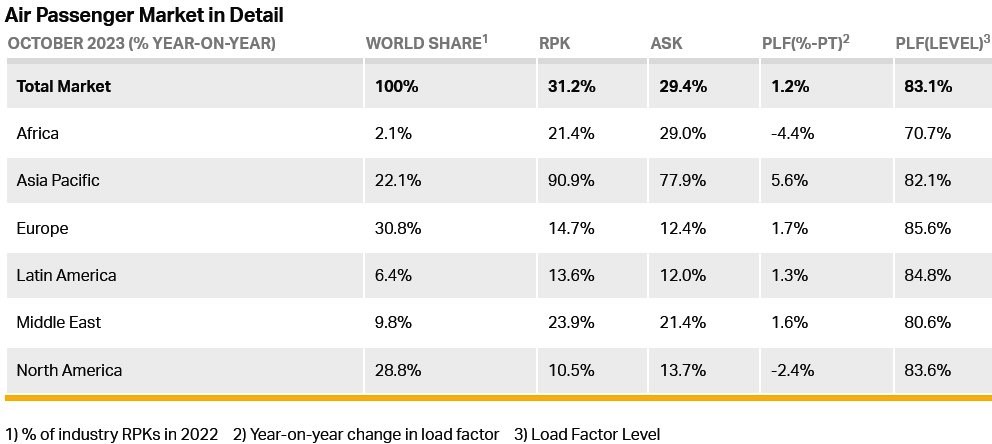

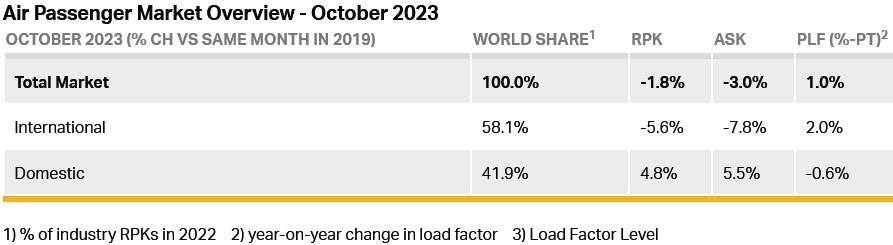

Total traffic in October 2023 (measured in revenue passenger kilometres or RPKs) rose 31.2% compared to October 2022. Globally, traffic is now at 98.2% of pre-COVID levels.

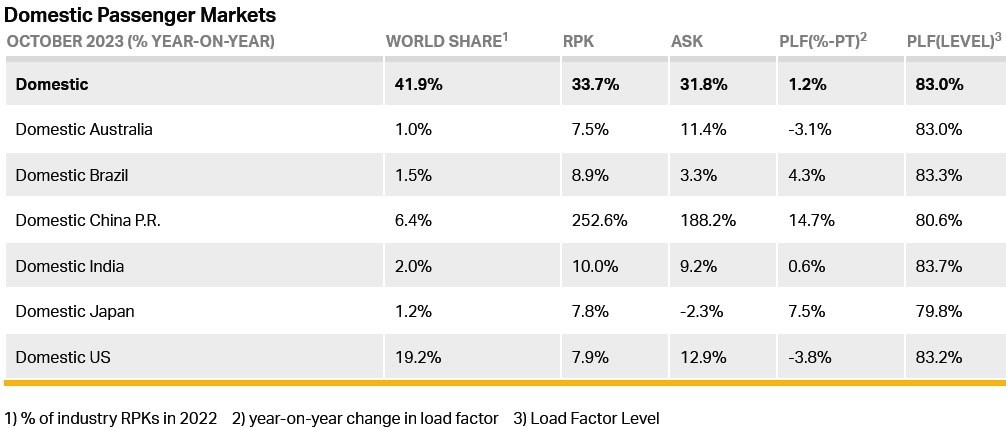

Domestic traffic for October rose 33.7% versus October 2022, driven by the triple-digit percentage growth recorded in China and was 4.8% above the October 2019 results.

International traffic climbed 29.7% compared to the same month a year ago. All markets saw double-digit percentage gains year on year. International RPKs reached 94.4% of October 2019 levels.

Willie Walsh (above), IATA’s Director General, said: “October’s strong result brings the industry ever closer to completing the post-pandemic traffic recovery. Domestic markets remain above pre-COVID levels. International demand is recovering, but more slowly. In particular, Asia Pacific carriers’ international demand is 19.5% behind 2019. This could reflect the late lifting of COVID restrictions in parts of the region as well as commercial developments and political tensions.”

International Passenger Markets

Asia-Pacific airlines saw an 80.3% increase in October 2023 traffic compared to October 2022, continuing to lead the regions. Capacity climbed 72.5% and the load factor increased by 3.6 percentage points to 82.9%.

European carriers’ October 2023 traffic rose 16.1% versus October 2022. Capacity increased 14.5%, and load factor edged up 1.2 percentage points to 85.1%,

Middle Eastern airlines posted a 24.1% rise in October 2023 traffic compared to a year ago. Capacity rose 22.2% and load factor climbed 1.2 percentage points to 80.6%. There was little impact at the regional and global levels from the Israel-Hamas war, despite reduced airline operations to/from Israel.

North American carriers had a 17.5% traffic rise in October 2023 versus the 2022 period. Capacity also increased 17.5%, and load factor was stable at 83.9%.

Latin American airlines’ traffic rose 21.2% compared to the same month in 2022. October capacity climbed faster -- up 22.3% -- pushing load factor down 0.8 percentage points to 85.3%, highest among the regions.

African airlines saw a 25.3% traffic increase in October 2023 versus a year ago. October capacity was up 32.4% causing load factor to decline 4.0 percentage points to 70.3%, lowest among the regions.

Brazil’s domestic RPKs rose 8.9% compared to a year ago and were 1.1% above the 2019 result.

US domestic demand climbed 7.9% in October but this was exceeded by a 12.9% rise in capacity, pushing domestic load factor down for a third straight month, to 83.2%.

Walsh said: “People assign a high value to the freedom to travel. The strong demand we’ve seen all year confirms that. And aviation is committed to ensuring that people can continue to enjoy this freedom. To do that in the long-term, we must also meet our commitment to achieve net zero carbon emissions by 2050. Last month, the Third Conference on Aviation Alternative Fuels (CAAF/3) agreed a global framework to promote Sustainable Aviation Fuel (SAF) production with the aim that aviation fuel in 2030 is 5% less carbon intensive than fossil fuel used today.

"Now, governments need to support that target by immediately putting in place policies to stimulate SAF production. It bears repeating: last year, every drop of SAF that was produced was purchased. The same thing will occur this year. But, with a few notable exceptions, governments are not living up to their obligations to ensure SAF is plentiful and affordable to support the industry’s energy transition.”

Cargo

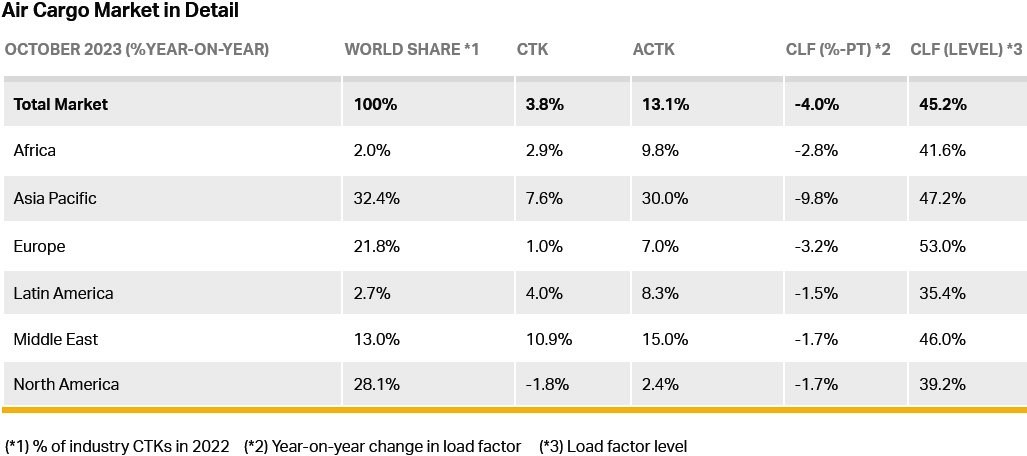

IATA data for October 2023 global air cargo markets reflects the third consecutive month of stronger year-on-year demand.

Global demand, measured in cargo tonne-kilometres (CTKs), increased by 3.8% compared to October 2022. For international operations, the demand lagged slightly at 3.5%.

Capacity, measured in available cargo tonne-kilometres (ACTKs), was up 13.1% compared to October 2022 (11.1% for international operations). This was largely related to the growth in belly capacity. International belly capacity, for example, rose 30.5% year-on-year on the strength of passenger markets.

Operating environment factors included:

- Economic activities slowed in October. With the Purchasing Managers’ Index for manufacturing output and export orders for major economies (excluding the US) remaining below the critical 50 mark, there is a clear marker for economic challenges ahead.

- Inflation in major advanced economies continued to ease from its peak in terms of Consumer Price Index (CPI), reaching between 3% and 4% for the US and for the EU respectively, in October. China’s CPI, however, indicated deflation for the second time this year, raising concerns of an economic slowdown.

- Global trade reversed its downward trajectory and stabilised in September. Although below its 2022 peak, global cross-border trade is more than 5% above pre-pandemic levels.

- After a continuous 17-month decline, cargo yields ticked-up in September and continued into October with a 2.6% month-on-month gain, remaining well-above pre-pandemic levels.

“Demand for air cargo was up 3.8% in October. That marks three consecutive months of year-on-year growth, placing air cargo on course to end 2023 on a much stronger footing than it began the year. Recovering demand, slightly stronger yields and the uptick in trade are all good news. But with demand still 2.4% below pre-pandemic levels, and much uncertainty remaining over the trajectory of the global economy, optimism must be balanced with caution. Nonetheless, a continued strong peak year-end season will certainly help the sector to manage through whatever turns the global economy might take in 2024,” said Walsh.

October Regional Performance

Asia-Pacific airlines saw their air cargo volumes increase by 7.6% in October 2023 compared to the same month in 2022. This performance was close to par with the previous month (+7.7%). Carriers in the region benefited from ongoing growth in international CTK’s on three major trade lanes: Africa-Asia (+16.7%, the greatest annual growth since May), Middle East-Asia (+10.3%) and Europe-Asia (+8.5%). Available capacity for the region’s airlines increased by 30.0% compared to October 2022 as more belly capacity came online from the passenger side of the business (a year ago, the key Asian markets of Japan and China were still largely under severe COVID-19 travel restrictions).