IATA sees strong air passenger and cargo demand growth for February

Image courtesy IATA

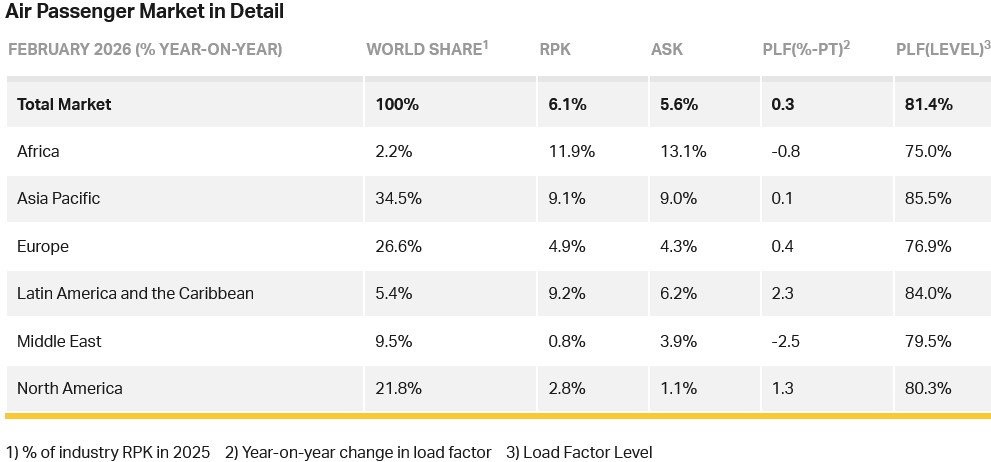

Total demand, measured in revenue passenger kilometres (RPK), was up 6.1% compared to February 2025. Total capacity, measured in available seat kilometres (ASK), increased 5.6% year-on-year.

The load factor was 81.4% (+0.3 ppt compared to February 2025), the highest February figure on record and international demand rose 5.9% compared to February 2025. Capacity was up 5.3% year-on-year, and the load factor was 80.5% (+0.5 ppt compared to February 2025).

Domestic demand increased 6.3% compared to February 2025. Capacity increased 6.2% year-on-year. The load factor was 82.8% (+0.1 ppt compared to February 2025).

Willie Walsh (above), IATA’s Director General, said: “With an RPK expansion of 6.1%, February was a strong month, showing that the fundamentals for demand growth were in place for a positive year. However, without knowing the length and intensity of the war in the Middle East, it is impossible to quantify the full impact that it will have on airline prospects. But some things are already clear. Fuel costs have risen sharply. With tight capacity and thin margins, air fares are already rising.

"Capacity deployment is also adjusting, particularly for traffic to, from, or through the Middle East, or in areas where fuel supply is an issue. Capacity growth scheduled for March, for example, has eased to 3.3% from earlier predictions of more than 5%.”

Regional Breakdown - International Passenger Markets

International RPK growth reached 5.9% in February compared to a year ago, with growth particularly strong in Latin America. Asia traffic benefited from the Lunar New Year travel demand. Traffic between Europe and Asia was especially robust (+14%), particularly between Asia and Spain and Italy.

Asia-Pacific airlines achieved an 8.6% year-on-year increase in demand. Capacity increased 7.3% year-on-year, and the load factor was 86.6% (+1.0 ppt compared to February 2025).

European carriers had a 5.0% year-on-year increase in demand. Capacity increased 4.5% year-on-year, and the load factor was 75.6% (+0.4 ppt compared to February 2025).

North American carriers saw a 5.0% year-on-year increase in demand. Capacity increased 2.4% year-on-year, and the load factor was 80.9% (+2.0 ppt compared to February 2025).

Middle Eastern carriers saw a 0.9% year-on-year increase in demand. Capacity increased 3.8% year-on-year, and the load factor was 79.6% (-2.2 ppt compared to February 2025).

Latin American airlines saw a 13.5% year-on-year increase in demand. Capacity climbed 9.3% year-on-year. The load factor was 85.0% (+3.1 ppt compared to February 2025).

African airlines saw a 4.8% year-on-year increase in demand. Capacity was up 6.6% year-on-year. The load factor was 74.5% (-1.3 ppt compared to February 2025).

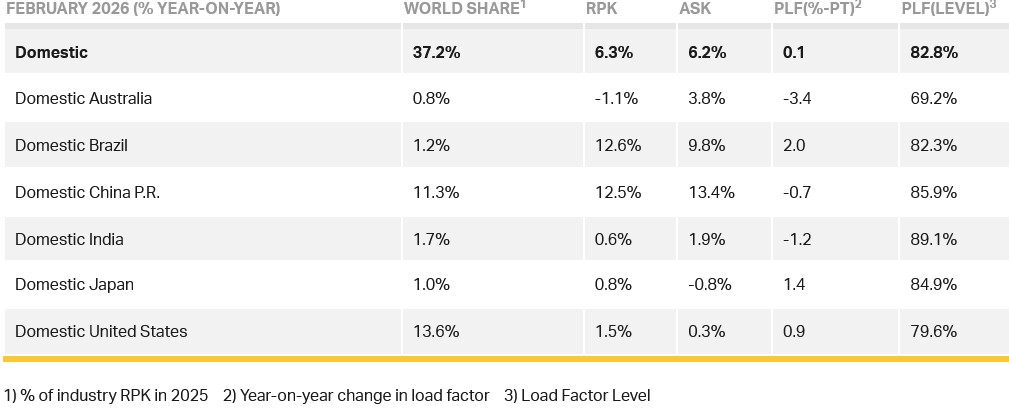

Domestic Passenger Markets

Domestic RPK rose by a robust 6.3%, driven by strong demand in Brazil and China. The capacity increase (+6.2%) was close to matching demand and the load factor was basically steady at 82.8%.

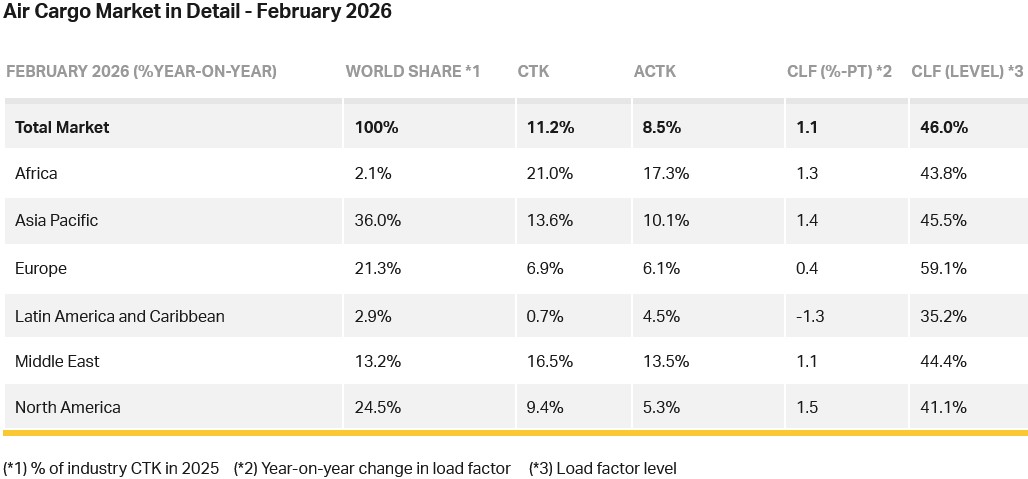

Air Cargo

IATA data for February 2026 global air cargo markets revealed total demand, measured in cargo tonne-kilometres (CTK), rose by 11.2% compared to February 2025 levels (+11.6% for international operations), whilst capacity, measured in available cargo tonne-kilometres (ACTK), increased by 8.5% compared to February 2025 (+9.8% for international operations).

Willie said: “Air cargo demand grew 11.2% in February. Even considering the boost that February received from the movement of goods ahead of Lunar New Year, the month showed strong growth. The outbreak of war in the Middle East at the end of the month, however, makes it difficult to see how full-year performance will unfold.

"Sharply rising fuel costs, fuel scarcity in parts of the world and the severe disruption to key cargo hubs in the Gulf are major shifts. While air cargo has repeatedly proven its resilience in the face of disruption, an early resolution of the war along with a normalisation of fuel supply and costs would be in everybody’s interest.”

Several factors in the operating environment should be noted:

- The global goods trade grew by 5.2% year-on-year in January.

- Jet fuel prices rose 1.2% year-on-year in February, while a widening Brent–jet fuel crack spread highlighted continued volatility in refining margins.

- Global manufacturing sentiment strengthened in February, with the Purchasing Managers’ Index (PMI) rising to 53.1, remaining above the 50-point expansion threshold. The PMI for new export orders rose to 51.4, above the growth threshold and the highest level since July 2021, indicating positive conditions for air cargo demand.

February Regional Performance

Asia-Pacific airlines saw a 13.6% year-on-year growth in air cargo demand in February. Capacity increased by 10.1% year-on-year.

North American carriers saw a 9.4% year-on-year increase in air cargo demand in February. Capacity increased by 5.3% year-on-year.

European carriers saw a 6.9% year-on-year increase in demand for air cargo in February. Capacity increased 6.1% year-on-year.

Middle Eastern carriers saw a 16.5% year-on-year increase in demand for air cargo in February. Capacity increased by 13.5% year-on-year.

Latin American and Caribbean carriers saw a 0.7% year-on-year increase in demand for air cargo in February, the weakest performance of all regions. Capacity increased by 4.5% year-on-year.

African airlines saw a 21.0% year-on-year increase in demand for air cargo in February, the strongest rise of all regions. Capacity increased by 17.3% year-on-year.

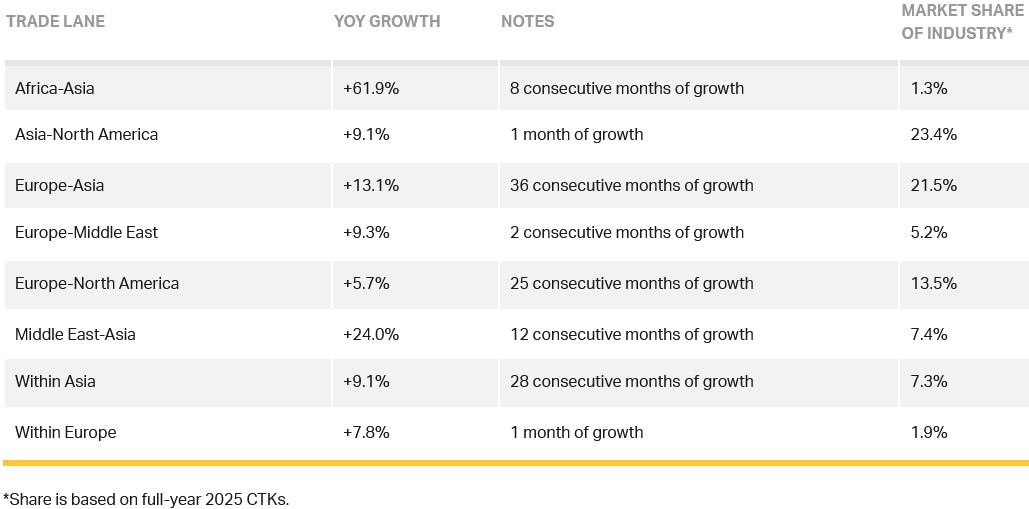

Trade Lane Growth

Air freight volumes in February 2026 increased across all major trade corridors.