Passenger numbers and cargo continue to recover

Image courtesy IATA

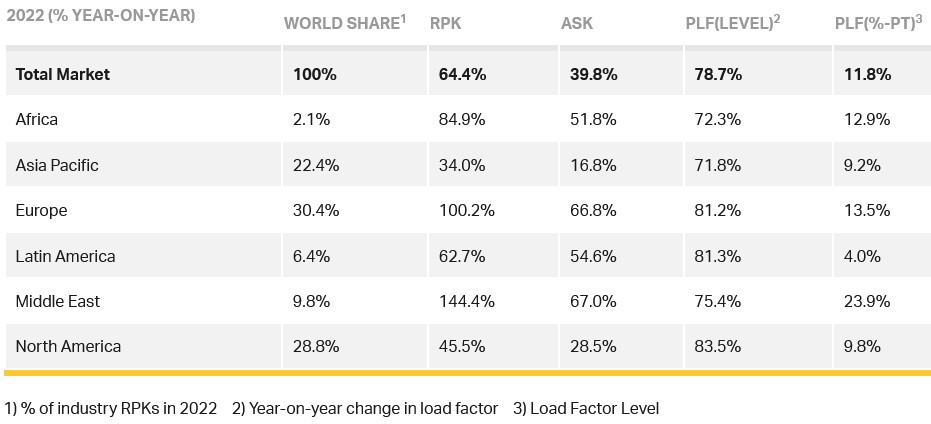

Total passenger traffic in 2022 (measured in revenue passenger kilometres or RPKs) rose 64.4% compared to 2021. Globally, full year 2022 traffic was at 68.5% of pre-pandemic (2019) levels. December 2022 total traffic rose 39.7% compared to December 2021 and reached 76.9% of the December 2019 level.

International traffic in 2022 climbed 152.7% versus 2021 and reached 62.2% of 2019 levels. December 2022 international traffic climbed 80.2% over December 2021, reaching 75.1% of the level in December 2019.

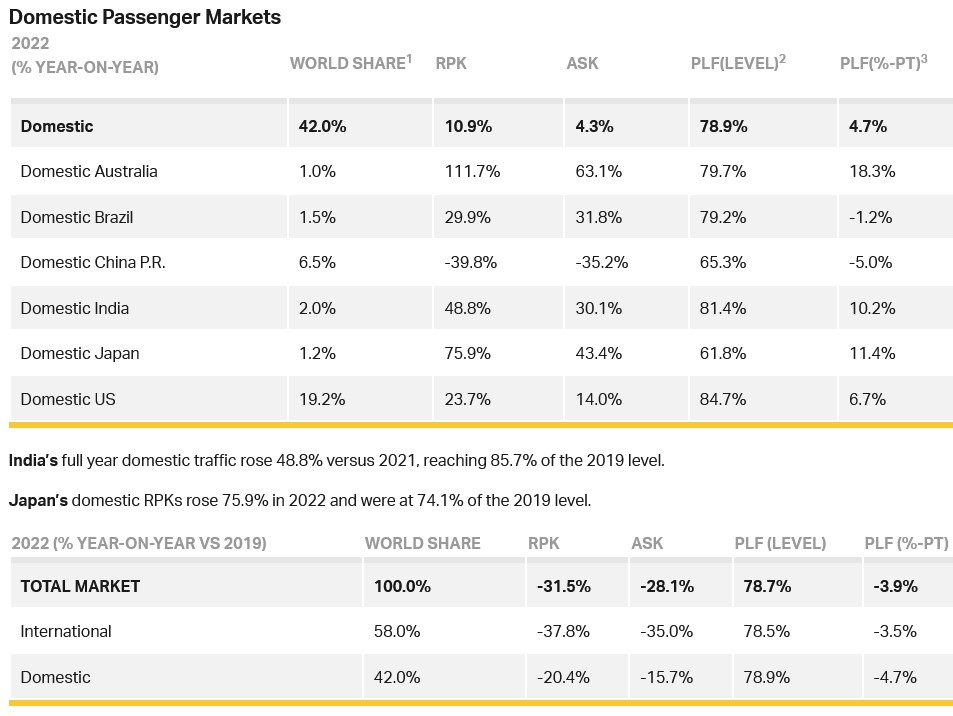

Domestic traffic for 2022 rose 10.9% compared to the prior year. 2022 domestic traffic was at 79.6% of the full year 2019 level. December 2022 domestic traffic was up 2.6% over the year earlier period and was at 79.9% of December 2019 traffic.

Willie Walsh (above), IATA’s Director General said: “The industry left 2022 in far stronger shape than it entered, as most governments lifted COVID-19 travel restrictions during the year and people took advantage of the restoration of their freedom to travel. This momentum is expected to continue in the New Year, despite some governments’ over-reactions to China’s re-opening.”

International Passenger Markets

Asia-Pacific airlines posted a 363.3% rise in full year international 2022 traffic compared to 2021, maintaining the strongest year-over-year rate among the regions. Capacity rose 129.9% and the load factor climbed 37.3 percentage points to 74.0%. December 2022 traffic rose 302.7% compared to December 2021.

European carriers’ full year traffic climbed 132.2% versus 2021. Capacity increased 84.0%, and load factor rose 16.7 percentage points to 80.6%. For December, demand climbed 46.5% compared to the same month in 2021.

Middle Eastern airlines saw a 157.4% traffic rise in 2022 compared to 2021. Capacity increased 73.8% and load factor climbed 24.6 percentage points to 75.8%. December demand climbed 69.8% compared to the same month in 2021.

North American carriers reported a 130.2% annual traffic rise in 2022 compared to 2021. Capacity increased 71.3%, and load factor climbed 20.7 percentage points to 80.8%. December 2022 traffic rose 61.3% compared to the year-ago period.

Latin American airlines posted a 119.2% traffic rise in 2022 over full year 2021. Annual capacity climbed 93.3% and load factor increased 9.7 percentage points to 82.2%, the highest among the regions. December demand climbed 37.0% compared to December 2021.

African airlines’ annual traffic rose 89.2% in 2022 versus the prior year. Full year 2022 capacity was up 51.0% and load factor climbed 14.5 percentage points to 71.7%, the lowest among regions. December 2022 traffic for African airlines rose 118.8% over the year-earlier period.

Walsh said: “Let us hope that 2022 becomes known as the year in which governments locked away forever the regulatory shackles that kept their citizens earthbound for so long. It is vital that governments learn the lesson that travel restrictions and border closures have little positive impact in terms of slowing the spread of infectious diseases in our globally inter-connected world. However, they have an enormous negative impact on people’s lives and livelihoods, as well as on the global economy that depends on the unfettered movement of people and goods.”

Cargo

Global full-year demand in 2022, measured in cargo tonne-kilometres (CTKs), was down 8.0% compared to 2021 (-8.2% for international operations). Compared to 2019, it was down 1.6% (both global and international).

Capacity in 2022, measured in available cargo tonne-kilometres (ACTKs), was 3.0% above 2021 (+4.5% for international operations). Compared to 2019 (pre-COVID) levels, capacity declined by 8.2% (-9.0% for international operations).

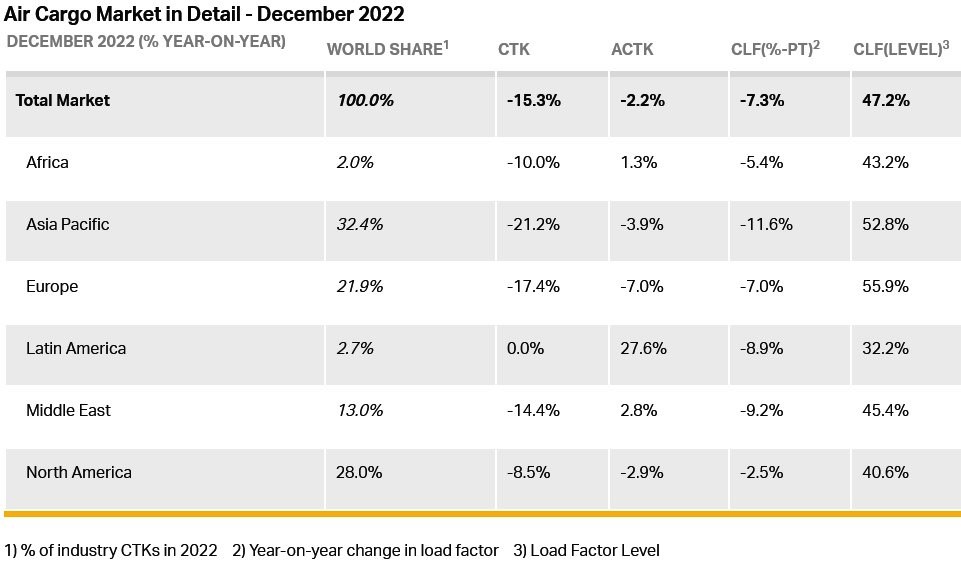

December saw a softening in performance: global demand was 15.3% below 2021 levels (-15.8% for international operations). Monthly cargo demand tracked below 2021 levels from March 2022. Global capacity was 2.2% below 2021 levels (‑0.5% for international operations). This was the tenth consecutive monthly contraction compared to 2021 performance.

2022 ended with mixed signals:

- Global new export orders, a leading indicator of cargo demand, have stayed at the same level since October. For major economies, new export orders are shrinking except in Germany, the US, and Japan, where they grew.

- Global goods trade decreased by 1.5% in November, down from a 3.4% increase in October.

- The Consumer Price Index for G7 countries indicated inflation tracking at 6.8% for December. The 0.6 percentage point drop compared to November (7.4%) was the largest over the course of year. Inflation in producer (input) prices reduced to 12.7% in October, its lowest level so far in 2022.

Walsh said: “In the face of significant political and economic uncertainties, air cargo performance declined compared to the extraordinary levels of 2021. That brought air cargo demand to1.6% below 2019 (pre-pandemic) levels.

"The continuing measures by key governments to fight inflation by cooling economies are expected to result in a further decline in cargo volumes in 2023 to -5.6% compared to 2019. It will, however, take time for these measures to bite into cargo rates. So, the good news for air cargo is that average yields and total revenue for 2023 should remain well above what they were pre-pandemic. That should provide some respite in what is likely to be a challenging trading environment in the year ahead.”

2022 Regional Performance

Asia-Pacific airlines posted an 8.8% decrease in demand in 2022 compared to 2021 (-7.4% for international operations) and a capacity increase of 0.5% (+5.8% for international operations). Compared to 2019 (pre-COVID levels), demand was 7.8% below (-3.9% for international operations) and capacity was down 17.2% (-12.2% for international operations). In December, Asia-Pacific airlines recorded the worst performance of all regions, posting a 21.2% decrease in demand (-20.4% for international operations) compared to 2021. Capacity fell 3.9% (-1.4% for international operations) during the same period. Airlines in the region continue to be impacted by lower levels of trade and manufacturing activity and disruptions in supply chains due to China’s rising COVID cases.

North American carriers reported a 5.1% decrease in demand in 2022 compared to 2021 (-6.3% for international operations) and a capacity increase of 4.2% (+4.9% for international operations). Compared to 2019 (pre-COVID levels), demand was 13.7% above (+12.7% for international operations) and capacity was up 8.2% (5.1% for international operations). In December, airlines in the region reported an 8.5% decrease in demand for both global and international operations, compared to 2021. Capacity fell 2.9% (+1.8% for international operations) during the same period.

European carriers posted the worst year-on-year performance of all regions, with an 11.5% decrease in demand in 2022 compared to 2021 (-11.8% for international operations). During the same period, airlines posted a capacity increase of 0.5% for both global and international operations. Compared to 2019 (pre-COVID levels), demand was 8.7% below (-9.1% for international operations) and capacity was down 16.5% (-17.3% for international operations). In December, airlines in the region posted a 17.4% decrease in demand (-17.9% for international operations) compared to 2021. Capacity fell 7.0% (-7.4% for international operations) during the same period. Airlines in the region continue to be most affected by the war in Ukraine.

Middle Eastern carriers reported a decrease of 10.7% for global and international demand in 2022 compared to 2021 and an increase in capacity of 4.3% (+4.5% for international operations). Compared to 2019 (pre-COVID levels), demand was 1.6% below for global and international operations and capacity was down 6.3% (-6.1% for international operations). In December airlines in the region posted a 14.4% decrease in demand for both global and international operations compared to 2021. Capacity increased 2.8% (+3.0% for international operations) during the same period.

Latin American carriers posted the strongest year-on-year performance of all regions, with an 13.1% increase in demand in 2022 compared to 2021 (+15.0% for international operations). During the same period, airlines posted a capacity increase of 27.1% (+27.8% for international operations). Compared to 2019 (pre-COVID levels), demand was 4.3% below (-2.6% for international operations) and capacity was down 14.3% (-10.8% for international operations). In December airlines in the region posted stagnant growth in demand (+2.3% for international operations) compared to 2021. Capacity grew 27.6% (+32.7% for international operations) during the same period.

African airlines reported a decrease in demand of 1.4% for global and international demand in 2022 compared to 2021 and an increase in capacity of 0.3% (-0.2% for international operations). Compared to 2019 (pre-COVID levels), demand was 8.3% above (+9.4% for international operations) and capacity was down 15.3% (-14.2% for international operations). In December, airlines in the region posted a 10.0% decrease in demand for both global and international operations compared to 2021. Capacity grew 1.3% (+0.2% for international operations) during the same period.